Insights

Q1 2026 Quarterly Newsletter

5 min read

Welcome to our Q1 2026 newsletter. To say that the first quarter of this year was eventful would be an understatement of historic proportions. In a matter of weeks, the world was reminded that the global economy is not just shaped by earnings reports and central bank decisions — it can be upended by geography, conflict, and the fragility of chokepoints most people couldn’t locate on a map.

Markets began the year on firm footing. Corporate earnings were strong, inflation had settled near 2.4%, and the broad mood was one of cautious optimism. Then, on February 28, 2026, the United States and Israel launched military strikes against Iran — and the world changed. Within days, Iran had closed the Strait of Hormuz, and roughly 20% of the world’s oil supply was cut off from global markets. WTI crude surged past $100 a barrel. Inflation jumped. Markets sold off. The IEA called it the “greatest threat to global energy security in history.”

This letter reviews what happened, what it means, and where we believe opportunity lies for the rest of 2026. But we want to lead with our central conviction:

The events of Q1 2026 have done more to vindicate the energy transition investment thesis than any policy announcement or corporate commitment ever could. Not because green energy is fashionable - but because dependence on fossil fuels that must pass through a 21-mile strait is now, unmistakably, a national liability. The world is repricing risk in real time.

Nor does the case rest on geopolitics alone. The explosive growth of artificial intelligence is creating an unprecedented surge in electricity demand - one the existing grid simply cannot meet. Data centers and GPU clusters powering the AI economy are projected to consume electricity at the scale of entire nations within this decade. That power must come from somewhere. The buildout of clean, reliable, domestic energy infrastructure - solar, wind, nuclear, battery storage, and grid modernization - is not just a climate story or a security story. It is the essential foundation upon which the AI economy will be built. These are the themes we are playing, and we believe they represent some of the most durable investment opportunities of this decade.

The Quarter at a Glance

After a solid start to the year — with January posting modest gains across all major U.S. indexes and small- and mid-cap stocks leading the way — the first quarter ended in the red. The culprit was not earnings, valuations, or Fed policy. It was geopolitics.

The S&P 500 finished Q1 with a total return of approximately −4.3%, its worst quarterly performance since Q1 2025. The Nasdaq 100 fared worse, dropping −5.8%, as technology mega-caps bore the brunt of the selloff. The Magnificent Seven — the group of mega-cap tech companies that dominated market returns in prior years — were anything but magnificent in Q1. All seven posted losses. Microsoft led the decline, falling 23.3% for the quarter and single-handedly subtracting 1.4 percentage points from the S&P 500.

The contrast between large-cap growth and everything else was stark. While the headline S&P 500 index fell 4.3%, smaller companies and value-oriented names held up well — or even gained. The Russell 2000 and the equal-weight S&P 500 each gained nearly +1% for the quarter. This is a reminder that index-level returns can be deceiving: diversified investors across company sizes and styles experienced a much more moderate quarter than the headlines suggested.

The Oil Surge: A Defining Market Event

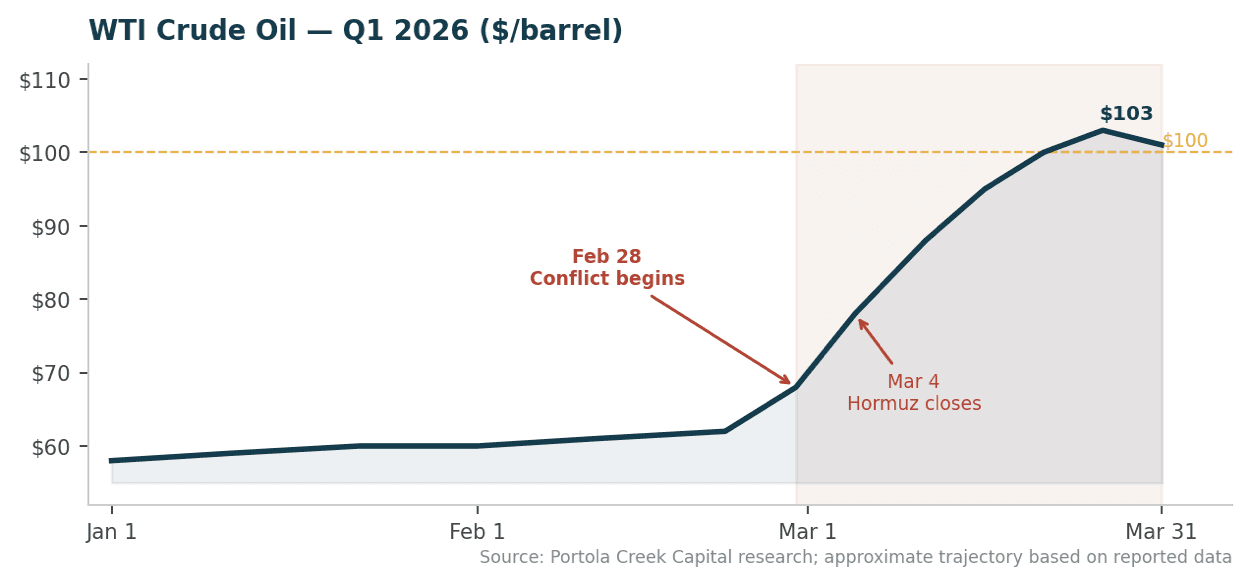

Oil prices rose more than 70% in Q1, moving from roughly $58 per barrel at year-end 2025 to above $100 by quarter-end — the highest level since 2022. This had cascading effects across the economy.

Gasoline prices at the pump rose approximately $1.00/gallon since late February.

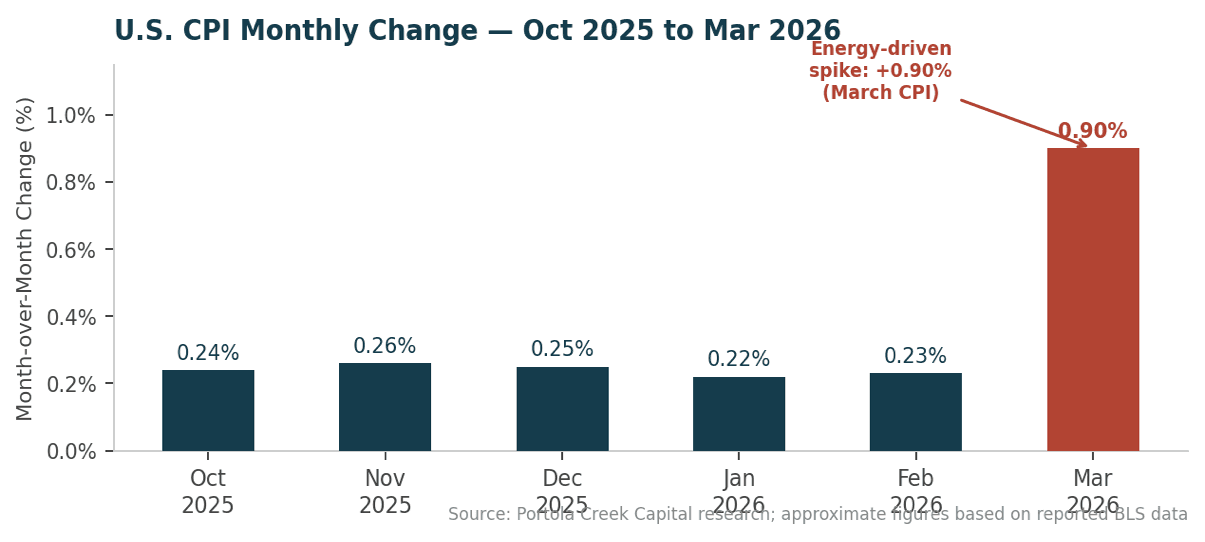

CPI, which had held steady at 2.4% through February, jumped to 3.3% in March — almost entirely driven by the energy component.

Rate cut expectations evaporated. Markets had priced in two to three Fed cuts in 2026 at the start of the year. By quarter end, none were expected.

Bond yields rose as inflation fears returned, pressuring the fixed income markets.

The IEA coordinated its largest-ever release of emergency oil reserves: 400 million barrels from member countries — a reprieve, not a cure.

A fragile ceasefire was reached in early April, and markets rallied sharply from their late-March lows — over 16% in just weeks. But the Strait of Hormuz remains effectively closed as of this writing, and the structural vulnerabilities revealed by this crisis will not be forgotten.

How It Began

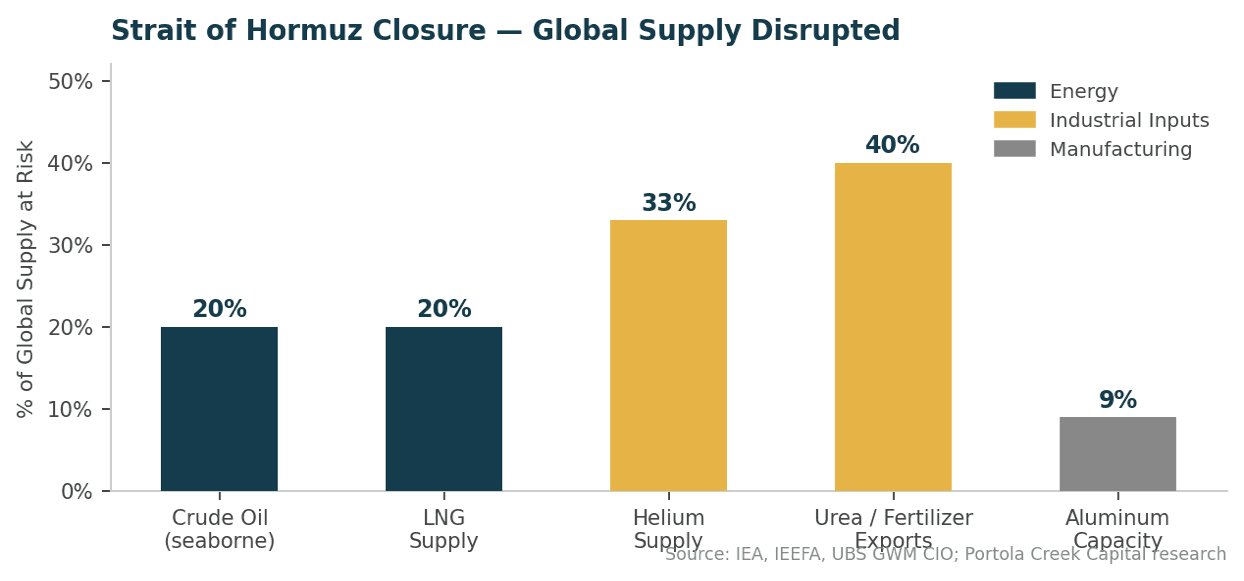

On February 28, 2026, U.S. and Israeli forces launched what was designated Operation Epic Fury — coordinated military strikes against Iranian nuclear and military infrastructure. Iran responded swiftly and decisively: by March 4, the Strait of Hormuz — the narrow 21-mile waterway between Iran and Oman through which roughly 20% of the world’s seaborne oil trade passes — was effectively closed to commercial traffic.

Crude oil and oil product flows through the Strait plunged from around 20 million barrels per day before the war to just over 2 million barrels per day by mid-March. The IEA’s executive director described it as the “greatest global energy security challenge in history.” Oil production from Kuwait, Iraq, Saudi Arabia, and the UAE collectively dropped by at least 10 million barrels per day by mid-March.

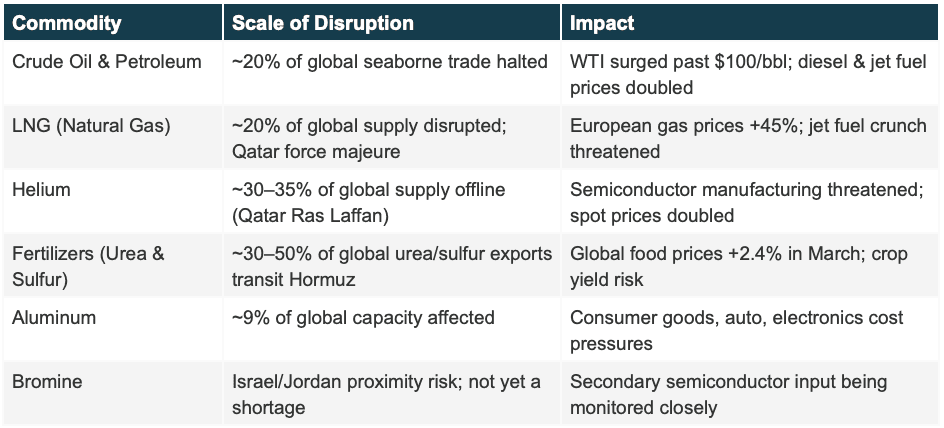

Not Just Oil: The Cascade of Disruptions

What made this crisis different from prior energy shocks was its breadth. The Strait of Hormuz is not just an oil artery — it is the world’s supply chain for multiple critical commodities:

The Gulf Humanitarian Crisis

The human and economic toll within the Gulf Cooperation Council (GCC) states has been severe. Countries like Kuwait, Qatar, and Bahrain rely on the Strait for the vast majority of their food imports — in Qatar, over 90% of food is imported. By mid-March, 70% of the region’s food imports were disrupted, triggering a grocery supply emergency. Iranian strikes on desalination plants — the source of 99% of drinking water in Kuwait and Qatar — escalated fears of a genuine humanitarian crisis. Food prices in Dubai reportedly spiked 40–120% for certain goods. The World Food Programme flagged long-term food security risks globally, given the scale of fertilizer disruption.

Meanwhile, Asian economies — which collectively absorb nearly 84% of crude oil transiting the Strait — faced acute shortages. Pakistan, Bangladesh, and Vietnam experienced severe fuel disruptions. India, the world’s fourth-largest oil refiner, moved quickly to source crude from Russia while installing piped gas connections to hundreds of thousands of new households in a single month. China, better insulated with 1.2 billion barrels in strategic reserves and a surging EV fleet, demonstrated that prior investment in energy diversification pays tangible dividends under exactly these conditions.

A One-Two Punch for Markets

Before the Iran conflict erupted, the economic narrative of early 2026 was already shaped by trade policy. The Trump administration continued its aggressive tariff posture, maintaining elevated duties on goods from China, Canada, and Mexico. Corporate earnings calls in January and February were laced with tariff-related warnings: Eestée Lauder flagged a $100 million headwind; aerospace and industrial manufacturers cited supply chain cost pressures. January layoff announcements from U.S. firms hit their highest level since 2009, more than double the prior year.

Then, in late January, the Supreme Court ruled 6–3 that broad tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful. The administration responded by imposing a temporary import duty under the Trade Act of 1974 and opening new Section 301 investigations — signaling that the direction of trade policy would not change, even if the legal mechanism did.

For investors, the practical message is this: tariffs are not going away. They are restructuring supply chains, raising input costs, and accelerating the trend toward regionalization and friend-shoring. Companies with lean, diversified supply chains and pricing power will navigate this environment better than those with concentrated exposure to tariff-affected trade routes.

International Markets: A Turning Point?

One of the quieter stories of Q1 was the relative outperformance of international equities. International stocks narrowly outperformed U.S. stocks in Q1 2026, continuing a trend that began in 2025. This matters because valuations outside the U.S. remain meaningfully more attractive: the Eurozone trades at roughly 14x forward earnings, emerging markets at 13x, compared to approximately 20x for the S&P 500. That valuation gap is significant, and it’s one of the reasons we have been increasingly attentive to international allocations.

Europe, in particular, entered this crisis in better shape than it handled the Russian gas shock of 2022 — because it deliberately invested in renewable energy capacity, diversified gas supply, and demand reduction. Those choices reduced exposure when the crisis hit. That lesson is not lost on policymakers or investors.

A Thesis Validated in Real Time

For years, the case for investing in the energy transition — solar, wind, battery storage, grid infrastructure, electric vehicles — rested on three pillars: climate urgency, declining costs, and supportive policy. Those were good reasons. They remain good reasons.

But Q1 2026 added a fourth pillar that is arguably more powerful than all the others combined: energy security. When a single 21-mile waterway can cut off 20% of the world’s oil supply, disrupting everything from gasoline prices in California to semiconductor manufacturing in Taiwan to food security in the Gulf, the vulnerabilities of fossil fuel dependence are no longer abstract. They are immediate, measurable, and politically radioactive.

The IEA’s executive director Fatih Birol was direct: “I expect nuclear power will get a boost. Renewables will grow very strongly — solar, wind and others. I expect electric cars will benefit from this.” SPAC issuance tied to the energy transition sector surged to $11.8 billion in Q1 2026, nearly four times the volume of Q1 2025. Public markets joined what venture capital had been betting on for years.

China’s Dividend on EV Investment

China entered this crisis having crossed 50% of its installed electricity capacity from non-fossil sources ahead of schedule. Its aggressive EV push has displaced over 1 million barrels per day of oil demand. When the Hormuz closure hit, China held an estimated 1.2 billion barrels in strategic oil reserves and had more fiscal room to respond than almost any other major economy. This is not coincidence — it is the direct result of a decade of deliberate investment in energy transition infrastructure. The contrast with more fossil-dependent economies, which faced sharper constraints and more disruptive outcomes, is instructive.

India’s experience offers a nuanced counterpoint. The country had crossed 50% installed electricity from non-fossil sources ahead of schedule — which limited pressure on the power system and reduced fiscal strain from energy subsidies. But India still spends $26.4 billion per year importing cooking gas alone, mostly through the Strait. The lesson: partial transition buys resilience. Full transition eliminates the chokepoint risk entirely.

Alternative Energy Pipelines and New Routes

Saudi Arabia and the UAE have limited pipeline capacity that bypasses the Strait. But Iran’s April attacks on Saudi Arabia’s East-West pipeline — cutting throughput by roughly 700,000 barrels per day — and drone strikes on the port of Fujairah showed that even those alternatives are vulnerable. Gulf producers are now actively exploring permanent new export routes. The crisis has fundamentally shifted the cost-benefit analysis: investments in alternative infrastructure that seemed impractical now look like existential necessities.

For investors, this creates opportunity in pipeline infrastructure, LNG terminal development outside the Gulf, offshore deepwater production in Africa and the Americas, and the full spectrum of clean energy technologies. The structural tailwinds for energy transition have just gotten considerably stronger.

The Problem Most Investors Are Missing

If oil was the headline story of Q1, helium was the footnote that could become a chapter. You may think of helium as the gas that fills party balloons. In the global economy, it is something else entirely: a non-substitutable industrial input for semiconductor manufacturing.

Helium is used in multiple critical stages of chip production — cooling silicon wafers during the etching process, acting as a carrier gas, and detecting leaks in vacuum systems. There is no practical industrial substitute. Qatar, before the war, produced roughly one-third of the world’s helium as a byproduct of LNG processing at its Ras Laffan complex — the world’s largest LNG facility. Iran’s March strikes on Ras Laffan knocked out that production. Combined with the Hormuz blockade stranding roughly one-third of the world’s specialized cryogenic helium containers — which can only hold liquid helium for approximately 45 days before it evaporates — the world is now facing what analysts are calling “Helium Shortage 5.0.”

The Stakes for the Tech Industry

The numbers are significant. Qatar’s Ras Laffan facility accounts for roughly 30–35% of global helium supply. The market is currently missing approximately 5.2 million cubic meters of helium per month. Spot prices have doubled since early March. Moody’s Ratings warned that helium disruptions are now threatening the semiconductor supply chains that underpin artificial intelligence and data center build-out, quantifying the exposed capital at $650 billion.

South Korean chipmakers Samsung and SK Hynix — which together account for 80% of the HBM memory market and 70% of DRAM — sourced 55% of their helium from Gulf nations in 2025. Taiwan’s TSMC, which manufactures roughly 90% of the world’s most advanced chips, imports 97% of its energy and sources 37% of its electricity from LNG flowing through the Strait. “The semiconductor industry will pay whatever they need to” to secure supply, according to one industry CEO — but paying more is not the same as having more. Semiconductor manufacturers have already indicated they will not meet their 2030 manufacturing goals.

The fertilizer story is equally important, if less discussed. Over 30% of global urea exports and significant volumes of sulfur — key fertilizer inputs — transit the Strait. Brazil, which accounts for nearly 60% of global soybean exports, is almost entirely dependent on imported fertilizers, with nearly half transiting Hormuz. A sustained fertilizer shortage could reduce crop yields and drive global food price inflation, particularly in developing economies.

Our Forward-Looking View

Market selloffs born of fear and uncertainty are, historically, some of the best buying opportunities for patient, long-term investors. The University of Michigan Consumer Sentiment Index fell to 53 in March — well below its long-run average of 77. Historically, readings that low have preceded average 12-month S&P 500 returns of over 24%. We are not forecasting that outcome — but we note that periods of fear and periods of opportunity tend to overlap.

Against this backdrop, here is how we are thinking about the remainder of 2026:

Sectors We Find Attractive

Clean Energy Infrastructure (Solar, Wind, Battery Storage, Grid Tech): The structural case has been materially strengthened by Q1 events. Look for companies with diversified manufacturing outside the Gulf, strong order books, and exposure to grid-scale storage. U.S. battery manufacturers continue to benefit from the 45X Advanced Manufacturing credit. International renewable developers are pivoting from early-stage projects toward cash-generating assets — a more attractive risk profile.

Nuclear Power: IEA’s Birol explicitly flagged nuclear as a beneficiary of the crisis. Given nuclear’s role as a carbon-free baseload power source that requires zero fossil fuel transit routes, expect renewed government support and accelerating project approvals.

Defense and Energy Security: Government defense budgets are rising globally. Drone and unmanned systems technology, cybersecurity for critical infrastructure, and AI-enabled defense applications are all seeing increased investment. The conflict has made energy security a top geopolitical priority.

Helium and Industrial Gases (non-Gulf sourced): The disruption to Qatari helium has been an unexpected catalyst for non-Gulf helium producers and industrial gas suppliers like Linde, which JPMorgan upgraded during the quarter and which has gained 15% in 2026. Companies building strategic helium reserves and recycling technologies are well-positioned.

Copper and Critical Minerals: The electrification buildout — EV charging networks, grid expansion, data center power infrastructure — requires enormous quantities of copper. Copper remains one of the most compelling commodity investment themes, with supply constrained by multi-year permitting cycles and rising project costs.

Gold: In a world of elevated geopolitical risk, higher inflation, and rising uncertainty about the dollar’s reserve role, gold continues to serve its purpose as a store of value and portfolio hedge.

Closing Thoughts

History tends to accelerate during moments of crisis. The geopolitical and economic disruptions of Q1 2026 have done exactly that — compressing what might have been a decade of energy policy evolution into a single quarter. The arguments that once seemed theoretical — that fossil fuel dependence is a systemic risk, that energy security and clean energy are the same investment thesis, that supply chain resilience is worth paying for — have been validated by events in the most visceral possible way.

We want to be clear about what this means for how we are investing on your behalf. We are not making panicked moves. We are not chasing the energy trade after a 70% oil surge. What we are doing is methodically building positions in the sectors and geographies where structural tailwinds are strong, valuations are reasonable, and the lessons of Q1 2026 are creating durable, long-term demand.

The ceasefire reached in early April is an encouraging sign. Markets have already recovered a substantial portion of their losses from the peak-to-trough drawdown. But the Strait of Hormuz remains effectively closed, the underlying geopolitical dynamics have not been resolved, and the world has been permanently reminded that the global fossil fuel system is fragile in ways that cannot be engineered away.

That reminder is the most powerful argument for the energy transition that has ever been made. And we intend to invest accordingly.

This newsletter is provided for informational and educational purposes only and does not constitute investment advice, a solicitation, or an offer to buy or sell any security. The information contained herein has been obtained from sources believed to be reliable, but Portola Creek Capital does not guarantee its accuracy or completeness. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. The views expressed herein represent the opinions of Portola Creek Capital’s investment team as of the date of publication and are subject to change without notice. Portola Creek Capital is not responsible for any errors or omissions in this publication. Please consult your financial advisor before making any investment decisions.